Non-Fungible Tokens (NFTs) Explained – what they are and how to use them

Content

Gone are the crazy days of CryptoKitties; Non-fungible Tokens (NFTs) have arrived in the real world. NFTs are seen as key to unlocking the market for collectibles which has an estimated global market size of 370 billion dollars (2020) and is expected to reach 520 billion dollars by 2028.

In May 2007, the digital artist known as Beeple set out to create and post a new work of art online every day. He hasn’t missed a day since, creating a new digital picture every day for 5 000 days straight. Individually known as EVERYDAYS, collectively, the pieces form the core of EVERYDAYS: THE FIRST 5000 DAYS, one of the most unique bodies of work to emerge in the history of digital art.

On March 11, 2021, British auction house Christies sold this piece of digital art for US$ 69.3 million to Metakovan, a pseudonym.

Metakovan, it turned out, was a crypto investor named Vignesh Sundaresan, who had recently bought 20 other Beeple NFTs, bundled them together, and offered portions of the bundle for sale via a blockchain token called B20. Sundaresan kept 59 percent of the B20 tokens; Beeple himself owned 2 percent. After that historic $69 million auction purchase put Beeple’s name in headlines around the world, the value of B20 tokens shot to a high of almost $25 – and then almost immediately plummeted. Today they're worth a few cents.

It is understandable why the average person might view N.F.T.s, as well as all crypto assets, such as cryptocurrencies, with suspicion, and possibly regard them as a complete scam.

Whereas everyone can look at or download this digital art, only Metakovan has ownership of this work (which he could sell at any time to another buyer). The NFT for it is a record on a cryptocurrency’s blockchain, in this case Ethereum.

In another instance, Twitter CEO Jack Dorsey’s first-ever tweet from 2006, which reads 'just setting up my twttr', was sold via an auction on the platform Valuables, which allows users to buy and sell autographed versions of tweets as an NFT.

Already we are seeing the applications of NFTs expand beyond digital art into categories such as video games, music, luxury fashion, domain names, and sports memorabilia. As a matter of fact, an NFT can be any type of one-of-a-kind digital asset, such as a video clip, text, virtual gaming assets, event ticket, or bits of code, where ownership of that asset is represented on a blockchain. The buyer of an NFT basically gets a crypto-backed digital receipt proving the NFT is authentic and that they own it.

Let’s delve deeper into how that vastly expanding universe of smart contracts actually works.

The Difference Between Fungible and Non-Fungible Tokens

The Merriam Webster dictionary defines the word fungible as 'being something (such as money or a commodity) of such a nature that another equal part or quantity may replace one part or quantity in paying a debt or settling an account'.

Currencies (e.g., US dollars) are fungible, i.e., when one person gives another person a five-dollar banknote, the other person can give back the original person a different five-dollar note. As long as the notes are genuine, they are exchangeable and have the same value.

In the digital world, the second generation of blockchain technology, which allows to program and execute software – so-called smart contracts, has led to the realization of new concepts designed to simplify human interaction and collaboration on a large scale across several industries such as supply chain management, international payments, international trade finance, energy markets, and notary services.

One particular development is the use cases of Initial Coin Offerings (ICOs) that re-invent crowdfunding through the use of blockchain and its ability to tokenize assets, enabled by the ERC-20 standard on the Ethereum platform. This standard, which specifies a common interface for fungible tokens that are divisible and not distinguishable, was mutually agreed on by the developer community to ensure interoperability. Fungible tokens can represent virtually anything:

- Reputation points in an online platform.

- Skills of a character in a game.

- Financial assets like a share in a company.

- A fiat currency like USD or EUR.

- An ounce of gold, a diamond, etc.

Fungible tokens cannot digitally represent uniqueness. In contrast, non-fungible tokens (NFTs) differ from fungible tokens (such as cryptocurrencies like Bitcoin) in two important aspects: Every NFT is unique, and it cannot be divided or merged.

Characteristics of an NFT

For a cryptographic token to be broadly classified as an NFT, it needs to follow four primary rules:

- It cannot be replicated.

- It cannot be counterfeited.

- It cannot be created on-demand.

- It possesses the same ownership rights and permanence guarantees as Bitcoin.

That means that each NFT represents something unique, authentic, and distinctive like collectibles. They have intrinsically different values and are not exchangeable. Furthermore, in the case of digital assets, a creator can also earn royalties each the NFT is sold or traded.

This new form of token was first introduced with the ERC-721 standard in late 2017 and further develop with ERC-1155 as standard interface for contracts that manage multiple token types. ERC-721 variates significantly from the ERC-20 standard as it extends the common interface for tokens by additional functions to ensure that tokens based on it are distinctly non-fungible and thus unique.

Full-history tradability, deep liquidity, and convenient interoperability enable NFT to become a promising intellectual property (IP)-protection solution.

Technical Components of NFTs

Blockchain

A blockchain is a decentralized ledger of records of transactions (called blocks) across a peer-to-peer network where participants stay anonymous. It’s called a chain because changes can be made only by adding new information to the end – which means that each new transaction grows the database. The most prevailing blockchain platform used in NFT schemes is Ethereum, providing a secure environment for executing the smart contracts.

Smart Contract

Most NFT solutions rely on smart contract based blockchain platforms to ensure their order-sensitive executions.

The basic idea of smart contracts is that many kinds of contractual clauses – such as liens, bonding, delineation of property rights, etc. – can be embedded in the hardware and software we deal with. The concept of smart contracts were originally introduced already in 1996, aiming to accelerate, verify or execute digital negotiation. Ethereum further developed smart contracts in the blockchain system.

Blockchain-based smart contracts adopt Turing-complete scripting languages to achieve complicated functionalities and execute thorough state transition replication over consensus algorithms to realize final consistency.

Smart contracts enable unfamiliar parties and decentralized participants to conduct fair exchanges without a trusted third party and further propose a united method to build applications across a wide range of industries.

Address and Transaction

Blockchain address and transaction are an essential concept in cryptocurrencies. A blockchain address is a unique identifier for a user to send and receive the assets, which is similar to a bank account when spending the assets in the bank. It consists of a fixed number of alphanumeric characters generated from a pair of public key and private key.

To transfer NFTs, the owner must prove in possession of the corresponding private key and send the assets to another address(es) with a correct digital signature. This simple operation is usually performed using a cryptocurrency wallet and is represented as sending a transaction to involve smart contracts in the ERC-777 token standard.

Establishing an NFT

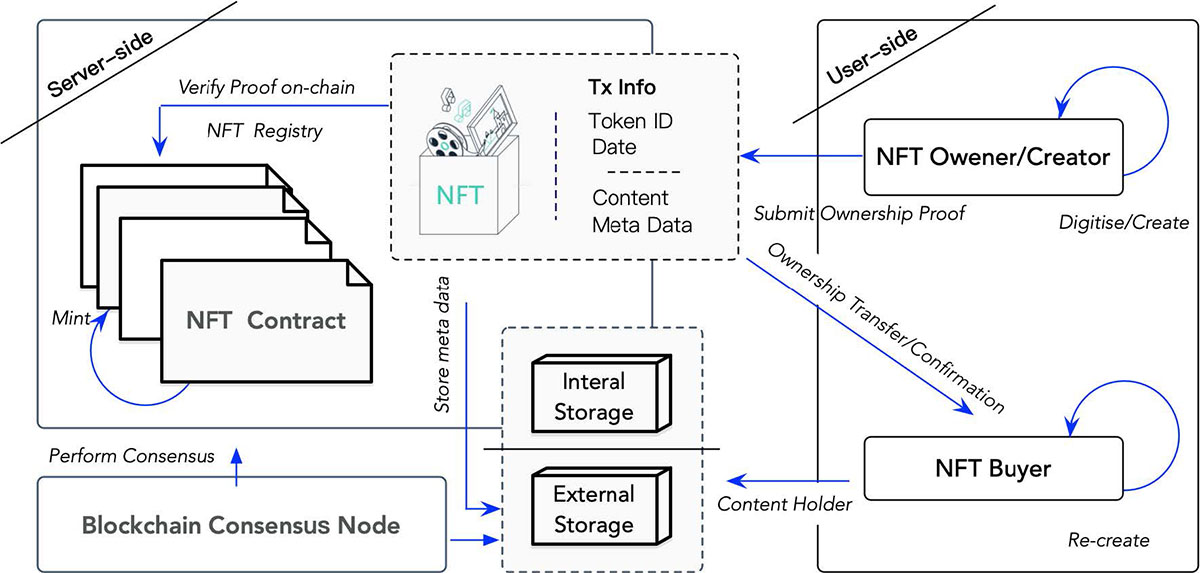

The establishment of NFT requires an underlying distributed ledger for records,

together with exchangeable transactions for trading in peer-to-peer network. The schematics above illustrates of the roles and components in an NFT transaction. Specifically:

1) NFT Digitizing. The NFT owner checks that file, title, and description are completely accurate. Then, they digitize the raw data into a proper format.

2) NFT Storage. The NFT owner stores the raw data into an external database outside the blockchain. Alternatively, they can store the raw data inside a blockchain.

3) NFT Signature. The NFT owner signs a transaction, including the hash of NFT data, and then sends the transaction to a smart contract.

4) NFT Minting & Trade. After the smart contract receives the transaction with the NFT data, the minting and trading process begins.

5) NFT Confirmation. Once the transaction is confirmed, the minting process is complete. From now on, the NFT will forever link to a unique blockchain address as its persistence evidence.

NFTs and Collectibles

NFTs have the potential to solve a tricky problem with digital art and other collectibles: how to exclusively own an original of something that can be downloaded, duplicated and shared freely on the internet. But collectors want the cachet – and are willing to pay for it – that comes with having an exclusive claim on an artwork. This is where NFTs come in.

To mint an NFT, the creator establishes a unique record of the artwork, generally on a website. Then the creator places the record on a blockchain, usually Ethereum’s, which requires a transaction fee known as gas. Gas refers to the fee required to conduct a transaction on Ethereum successfully. It is a unit that measures the amount of computational effort required to execute specific operations on the Ethereum network.

Possession of a private encryption key associated with the transaction proves ownership. This gives an artist or collector something to sell. An NFT may link to a version of the work, but rarely includes the rights to reproduce or distribute it. That differentiates it from a commercial licensing arrangement.

NFTs have quite a few problems, though. They usually are traded using cryptocurrencies, many of which can fluctuate in value like an out-of-control rollercoaster. Furthermore, anyone can mint an NFT which, doing so with someone else’s work, could be infringe their copyright. Some artists have already claimed misappropriation of their work. Most NFTs are simply links to images. Unless they have been issued in a certain way to ensure they are tamper-proof these can in theory be meddled with after the sale.

If you want to dig deeper into this area of NFT-based digital art markets we recommend this excellent paper: Virtual Art and Non-fungible Tokens.

NFTs in Gaming

NFT has great potential in the gaming industry. Among the quickly growing breeds of crypto games are not only classics like CrytpoKitties and Cryptocats but numerous newer entries like CryptoPunks, Axie Infinity, Gods Unchanged, Splinterlands, Alien Worlds, Battle Racers, TradeStars and many more.

By launching a game on blockchains and anchoring them with NFTs, a game gives players more control over in-game assets like lives, skins, characters, coins, weapons, virtual real estate and so on and allows to preserve the rarity and uniqueness of some of these in-game items.

In NFT games, players claim exclusive ownership of game assets through three main strategies – creating or breeding new characters; purchasing digital items in-game or on third-party marketplaces; or unlocking and earning new items. Games that provide blockchain-based ownership records allows players to sell their assets for NFTs. This is why this gaming model is called play-to-earn.

One fascinating feature of such games is the breeding mechanism. Users can personally raise pets and spend much time breeding new offspring. They can also purchase the limited/rare edition virtual pets, and then sell them at a high price.

Another attractive feature for NFT game developers is that they can royalties each time their items (e.g., weapons and skins) are (re-)sold on the open market.

NFT Event Ticketing

Tickets, whether as physical paper or electronically readable codes (note that QR-codes or barcodes only encode information but do not encrypt) on smartphones and watches, represent a mechanism to demonstrate entitlement to access to any event such as sports or culture. Tickets are sold directly by the event organizer or by authorized ticket agencies. Tickets for popular events are also resold on third-party marketplaces such as eBay. This ticket resale is a rapidly growing market and counterfeit, or invalidated tickets, are a problem growing with it.

NFT-based tickets are minted by the event organizer onto their blockchain of choice and they demonstrate entitlement to access to any event such as culture or sports. An NFT-based ticket is unique, preventing scams and fake tickets. The blockchain-based smart contract provides a transparent ticket trading platform for the stakeholders such as the event organizer and the customer.

Ticket issuers can also program their NFT tickets with rules for resales and merchandising deals (for instance merchandise discounts or reward points tied to the ticket). For instance, an event organizer can set a profit-sharing percentage for any re-sale of the ticket on secondary markets and reliably receive these funds. Even used NFT tickets can become collectables after the event.

NFTs in the Travel Industry

Tokenizing travel tickets has benefits for both travelers and travel companies like airlines and hotels. Can’t make a flight? Auction off your boarding pass on the secondary market. Need to change travel dates? Offer a premium to anyone who’s willing to trade tickets with you. In both cases, the travel companies could potentially get a cut, too.

The ability to auction, trade, swap, and transfer tickets from wallet to wallet gives travelers more control over how they manage their travel passes and potentially helps them avoid cancellation or rebooking fees.

NFT Trading Marketplaces

Using Blockchain technology, a company called WiV has created a solution to the logistical and authentication issues plaguing physical real-world assets. By transforming cases and bottles of wine in NFTs, they can create a provenance standard by making the wine’s history fully transparent and allowing digital transfer of ownership.

Other noteworthy marketplaces are:

For buying and selling digital art there are quite a few marketplaces: OpenSea, SuperRare, MakersPlace, VIV3.

Decentraland is a virtual world where you can buy and sell virtual real estate. Other metaverses are Cryptovoxels, Somnium Space, MegaCryptoPolis and Sandbox.

On Topshot you can collect and trade officially licensed NBA and WNBA digital Moments™.

Icecap, an Ethereum-based diamond NFT marketplace. You trade the tokens without friction while the diamonds are vaulted and insured.

Even NFT postage stamps are a thing now. For instance, the Crypto stamp is a physical postage stamp with an embedded NFC chip that has a digital twin in the blockchain. You can also create a Crypto stamp collection and trade your NFT stamps.

How to Create your Own NFTs

Some marketplaces like Mintable and Mintbase also provide their users with simple tools to turn their digital content into NFTs.

Creating an NFT cost you money: you’ll need to pay a platform to mint an NFT of your work. Most platforms want paying in Ether, the native cryptocurrency of blockchain platform Ethereum. Other NFT platforms include OpenSea, SuperRare, Nifty Gateway, Foundation, VIV3, BakerySwap, Axie Marketplace and NFT ShowRoom. Other payment platforms include Torus, Portis, WalletConnect, Coinbase, MyEtherWallet and Fortmatic.

First, you need to create a digital wallet and deposit some cryptocurrency into it. Then you connect your wallet to an NFT marketplace platform. Then you upload your digital file like JPEGs, PNGs, MP4s, PDFs, etc. Then you need to choose how you want to sell your NFT artwork. Commonly there are three options (pretty similar to what you can do on eBay): fixed price, unlimited auction (allowing people to carry on making bids until you accept one), and timed auction that runs for a certain time period that you determine. You also need to provide a description of your NFT (again, similar to how you prepare an item for sale on eBay).

A word on fees: In addition to the minting fee, you will incur a listing fee on the marketplace platform and a transaction fee for transferring the money from the buyer’s wallet to your own (gas fees). Make sure you understand the fee structures before you commit. There are also blockchains wit low or no gas fees, for instance Polygon.

We have created a collection of NFTs here at Nanowerk as well, go check it out at our Giants of Nanotech collection.

NFT Challenges

Some typical challenges with the use of today’s blockchain platforms concern usability, security, governance, and extensibility.

Most of NFT schemes are built on top of Ethereum. Therefore, it is obvious that the main drawbacks of Ethereum are inherited: slow confirmation and high gas prices. Other platforms do not charge for minting until the NFT is transferred on-chain when the first purchase or transfer is made.

Another very real risk concerns the fact that the content or metadata on an NFTs can simply ‘disappear’. This can happen because only the smart contract, the deed, is stored on the blockchain; the actual physical property (for instance a digital image or a video) is stored elsewhere, mainly because it’s either too large or onerous to store on the blockchain. That means that the contract continues to exist even when the underlying asset is gone.

You can use online tools like checkmynft.com to see where your NFT assets are stored.

For example, the token with the smart contract might not link directly to the asset. Or the asset could be on the servers of a hosting or cloud storage that could eventually shut down. And the NFT could merely link to a URL, which means that whatever is stored from that URL can be changed.

Point in case: Musical artist and blockchain enthusiast 3LAU has sold a music album for $11 million on the Ethereum blockchain. The album was sold as 33 NFTs on Origin Protocol's Dshop marketplace. And now it seems to be missing… To be sure, you can still find a copy of it on NiftyGateway, but the actual NFT asset appears to be no longer discoverable online. It exists only on a centralized provider, a business that could eventually go bust.

While the integrity of blockchain distributed ledger technology seems to hold at this point, several entities actually holding blockchain assets have been breached. One example of a smart-contract-based attack happened on Ethereum in June 2016, when about $60 million was stolen. More recently, customers of cryptocurrency company Coinbase suffered from a similar hack, resulting in ‘drained accounts’.

A final point on NFT challenges concerns extensibility – cross-chain interoperability and applications of blockchain updates.

Existing NFT ecosystems are isolated from each other. Users once have selected one type of product can only sell/buy/trade them within the same ecosystem/network. This is due to the reason of its underlying blockchain platform. Interoperability and cross-chain communication are always the handicaps for the wide adoption of decentralized apps (DApps).

Blockchains periodically update their protocols through soft forks (minor modifications that are compatible forwards) and hard forks (significant modifications that may conflict with previous protocols). Updating an existing blockchain could result in difficulties and trade-offs.

Check out our SmartWorlder section to read more about smart technologies.